Services

Wage Loss Replacement Plans

A Strategic Disability Solution for High-Income Employees and Executives

For many high-income employees and executives, traditional group disability plans do not provide sufficient income protection. Plan maximums and design limitations often result in a significant shortfall if a disability occurs.

A Wage Loss Replacement Plan (WLRP) is designed to address this gap by supplementing existing group disability coverage and providing more meaningful income replacement for key individuals. While these plans are most commonly used to supplement group Long-Term Disability (LTD), they can also be implemented on a stand-alone, grouped basis where no group LTD plan exists.

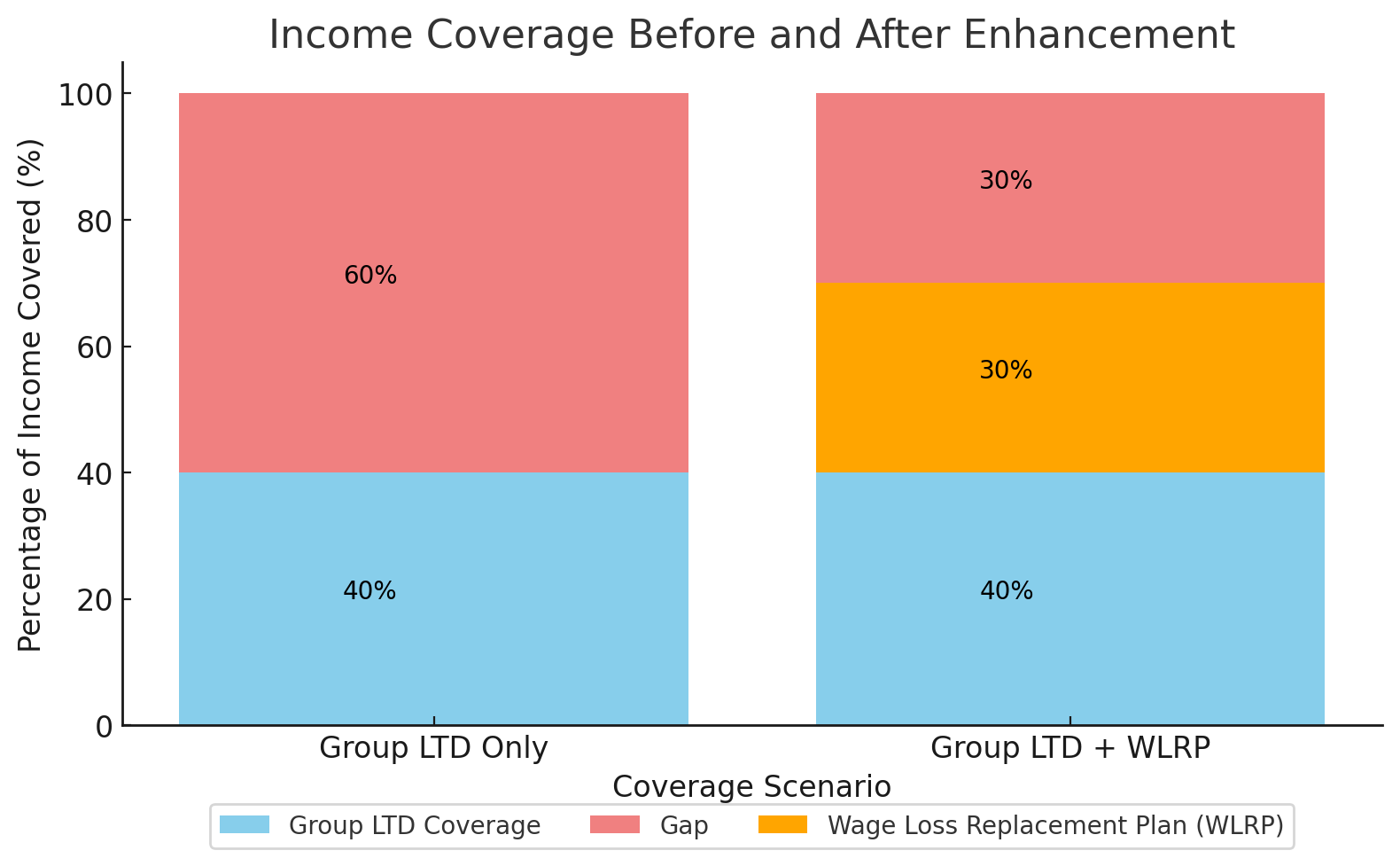

Why Wage Loss Replacement Plans Are Used

Group Long-Term Disability plans are typically structured to cover a percentage of income up to a maximum monthly benefit. For higher earners, this can leave a large portion of income uninsured.

A Wage Loss Replacement Plan can help:

- Improve overall income replacement for key employees

- Address benefit caps within traditional group LTD plans

- Provide more predictable financial outcomes during a disability

- Support business continuity by protecting critical individuals

The goal is not excess coverage, but appropriately aligned protection.

How Wage Loss Replacement Plans Work

A WLRP often operates alongside an existing group disability plan.

For example, an executive earning $250,000 per year may receive $5,000 per month from a standard group LTD plan. A Wage Loss Replacement Plan can be layered on top to increase total income replacement closer to an appropriate percentage of pre-disability earnings.

Benefits under a WLRP are typically taxable, as premiums are paid by the employer. Coverage amounts are therefore often structured at a higher level to account for taxation and achieve the desired after-tax outcome.

Tax Considerations

When structured properly:

- Premiums paid by the employer are generally deductible as a business expense

- Disability benefits paid to the employee are taxable

- The structure can be more efficient than increasing salary to fund personal disability coverage

Because tax treatment and plan design are closely linked, Wage Loss Replacement Plans require careful coordination with accounting and legal advisors.

Plan Design and Eligibility

Wage Loss Replacement Plans are not one-size-fits-all. Key considerations include:

- Which employees or classes are eligible

- Benefit percentages and maximums

- Coordination with existing group LTD coverage

- Consistency with overall compensation and benefits strategy

These plans are most commonly used for executives, partners, and other high-income or key individuals.

When a Wage Loss Replacement Plan Makes Sense

A Wage Loss Replacement Plan may be appropriate when:

- Group disability coverage leaves a meaningful income gap

- The business wants to protect key individuals without relying on Group LTD insurance alone

- There is a desire to improve benefits in a tax-aware manner

- Consistency and predictability of coverage are important

It is not appropriate in every situation, which is why design and implementation matter.

Final Thoughts

Wage Loss Replacement Plans are a specialized disability planning tool. When used correctly, they can significantly improve income protection for high-income employees while aligning with a company’s broader benefits and compensation strategy.

As with all disability planning, the value comes from understanding the exposure first, then selecting the right solution.

If you’d like to explore whether a Wage Loss Replacement Plan is appropriate for your organization, we’re happy to review your existing coverage and outline the options.

We would love to discuss your lifestyle and insurance needs.

No high pressure sales tactics. We simply educate you on making the best decision for you. We proudly serve Ontario, Alberta, and British Columbia.

We have adopted a proven systematic approach to working with clients virtually, which allows us to get to know our clients and help them make an informed decision on what insurance solution is best for them.